AllDefi Research · DeFi Yield Strategy Series (1/N)

TL;DR

- Looping is spread arbitrage, not directional leverage.

- Leverage is determined by LTV. Stablecoin pairs can reach 10x or higher.

- What actually causes looping positions to lose money or get liquidated falls into four categories: rate spikes, stablecoin depegs, liquidity shortages, and mass liquidations.

- On-chain looping is highly concentrated. Your liquidation price is effectively set by the entire market, not by you.

- The return structure of looping is clean, but the cost and risk of managing it manually exceeds what most participants can realistically handle.

1. A Strange Position On-Chain

Open Aave’s largest positions and a strange pattern keeps showing up:

The same address holds tens of millions in USDe — and borrows nearly the same amount in USDT.

Why would anyone deposit funds only to borrow them back? It’s not a bug. It’s not a mistake.

It’s one of DeFi’s most common — and most underestimated — strategies: looping, also known as recursive borrowing.

2. What Looping Actually Does

Using USDe / USDT as an example:

- You deposit 100 USDe and earn native yield on it (for example, Ethena’s yield).

- The protocol lets you borrow up to 90% of the collateral value as USDT, so you borrow 90 USDT.

- You swap that 90 USDT back into USDe (they trade near 1:1) and deposit it again.

- You borrow another 81 USDT, swap, deposit. Repeat.

After 5–6 rounds, your on-chain USDe deposit is roughly 5–7x the original. Your debt is around 4–6x. Your net principal is still 100 USDe.

Important: this is not “the same dollar used many times.” Every round of USDT borrowed is a real debt. Every round of USDe deposited is real collateral, locked up on-chain. What’s happening is that these deposits and debts together support a yield structure whose spread is much larger than the original principal.

What looping really does is let the same net principal carry the largest possible spread exposure.

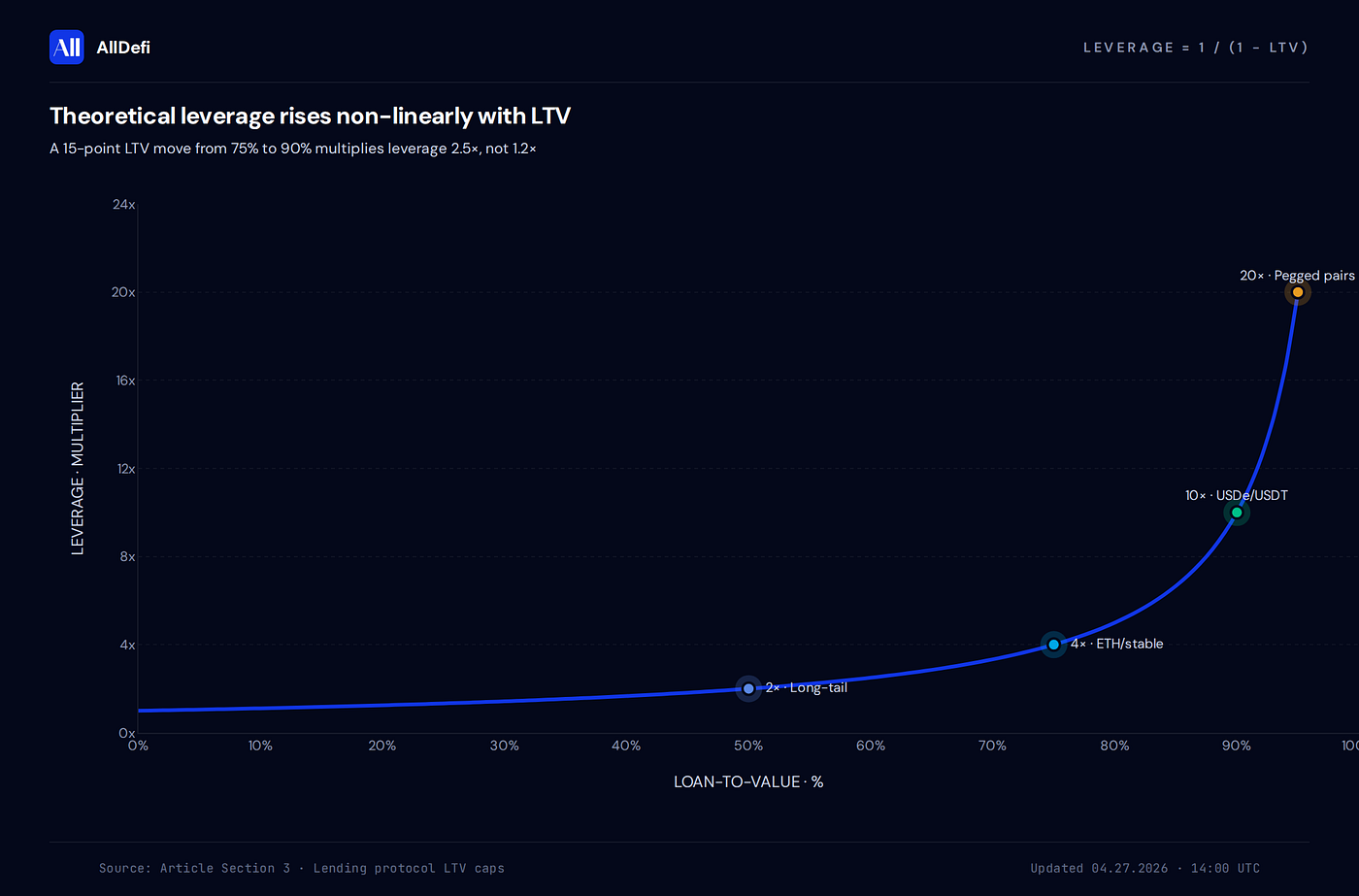

3. The Math of Leverage

Lending protocols set a cap called LTV (loan-to-value): the maximum you can borrow against your collateral.

After infinite recursion, the theoretical leverage is:

Leverage = 1 / (1 − LTV)

- 50% LTV (2x Leverage): Typical for long-tail collateral.

- 75% LTV (4x Leverage): Typical for ETH / stablecoin pairs.

- 90% LTV (10x Leverage): Typical for stablecoin pairs (e.g., USDe / USDT).

- 95% LTV (20x Leverage): Typical for strongly pegged pairs.

Stablecoin pairs can command 90%+ LTV because protocols assume their prices stay pegged.

In practice, almost no one loops to the limit. Most operators stop at 5–7 rounds, because each additional round contributes less yield while gas and slippage add up.

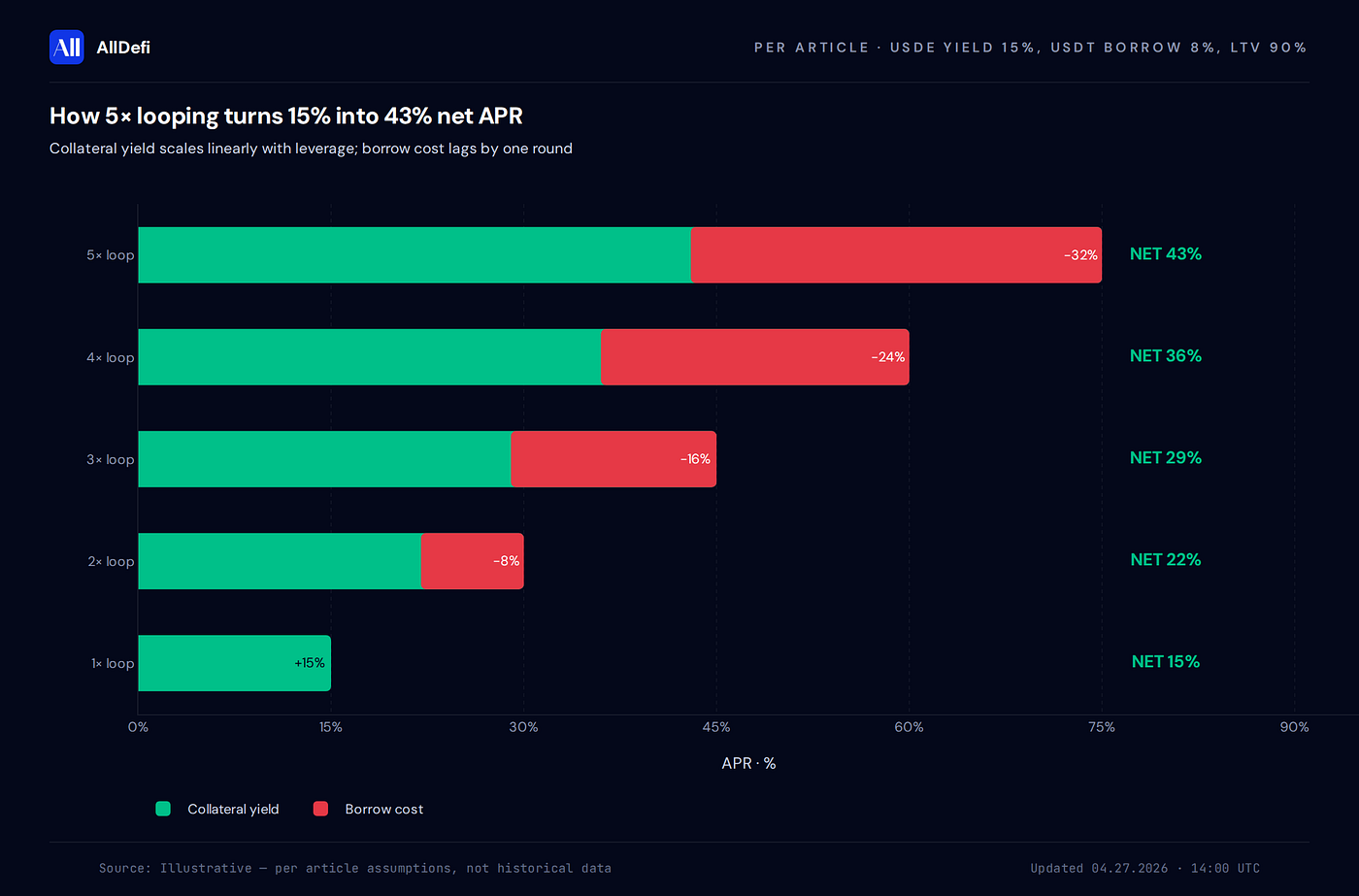

4. How Much Does It Earn?

Take an illustrative set of numbers (USDe / USDT):

- USDe native yield: 15%

- USDT borrow rate: 8%

- LTV: 90%

Without looping: 15%.

With 5x looping:

- Collateral side earns 5 × 15% = 75%

- Debt side pays 4 × 8% = 32%

- Net APR ≈ 43%

From 15% to 43% — this is the appeal of looping.

But neither of those rates is fixed. They move every day.

5. The Four Things That Actually Break Looping Positions

Newcomers think the risk of looping is “high leverage, easy liquidation.” Liquidation is the outcome. What actually triggers losses or forced exits comes down to these four.

They share a common feature: they move faster than any human response time.

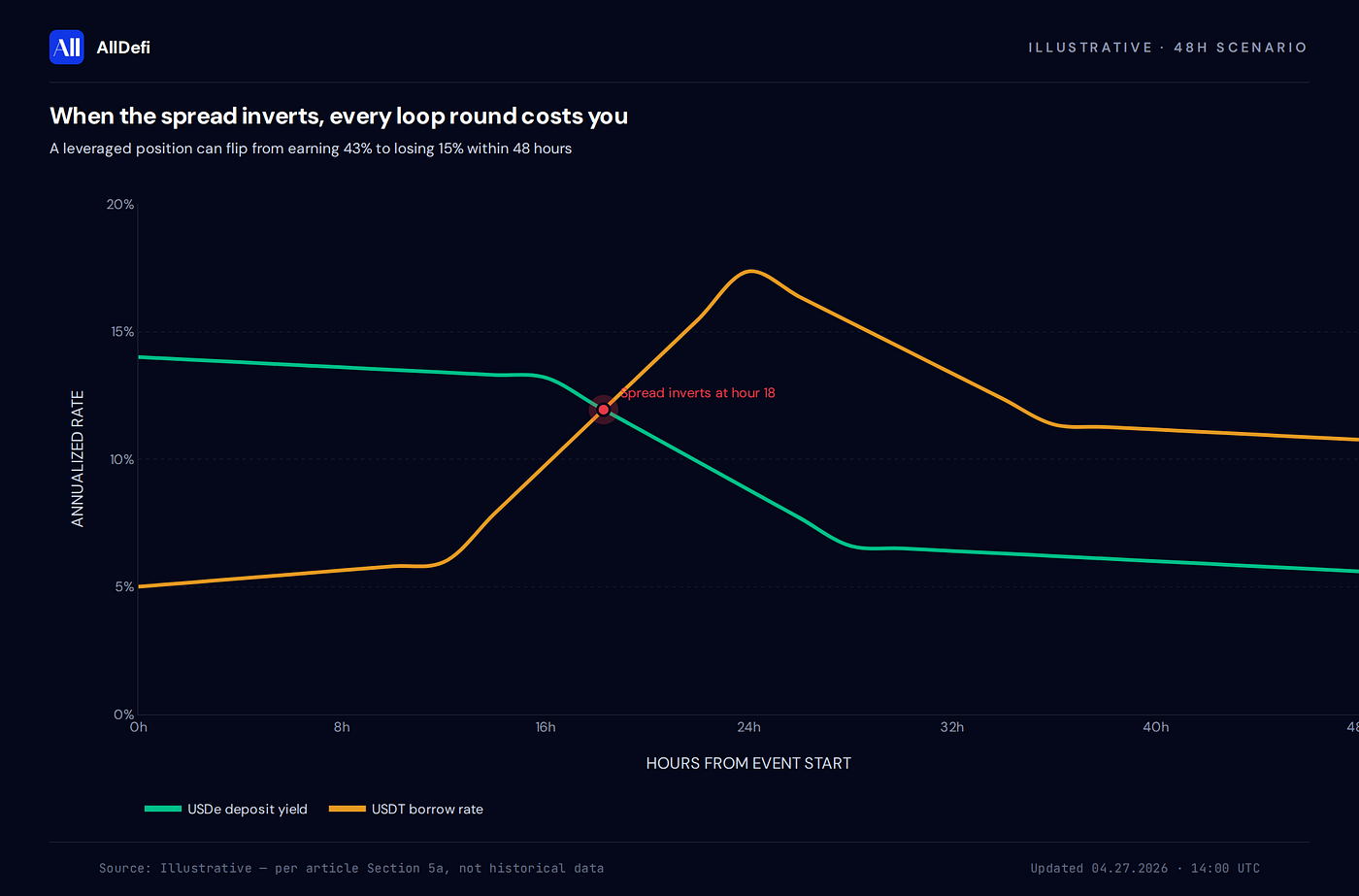

a. Borrow Rate Spikes

Lending protocol rates are driven by pool utilization. When capital floods into the same loop strategy, borrow demand surges and the borrow rate can jump from 5% to 15% — or 20% — within hours.

Once the borrow rate catches up to or exceeds your deposit yield, every loop round costs you money. The higher your leverage, the faster you bleed.

The USDe / USDT spread has collapsed from +9% to −3% in 48 hours. The same position went from earning 43% to losing 15%.

By the time you notice and manually unwind, the worst of it is already two days behind you.

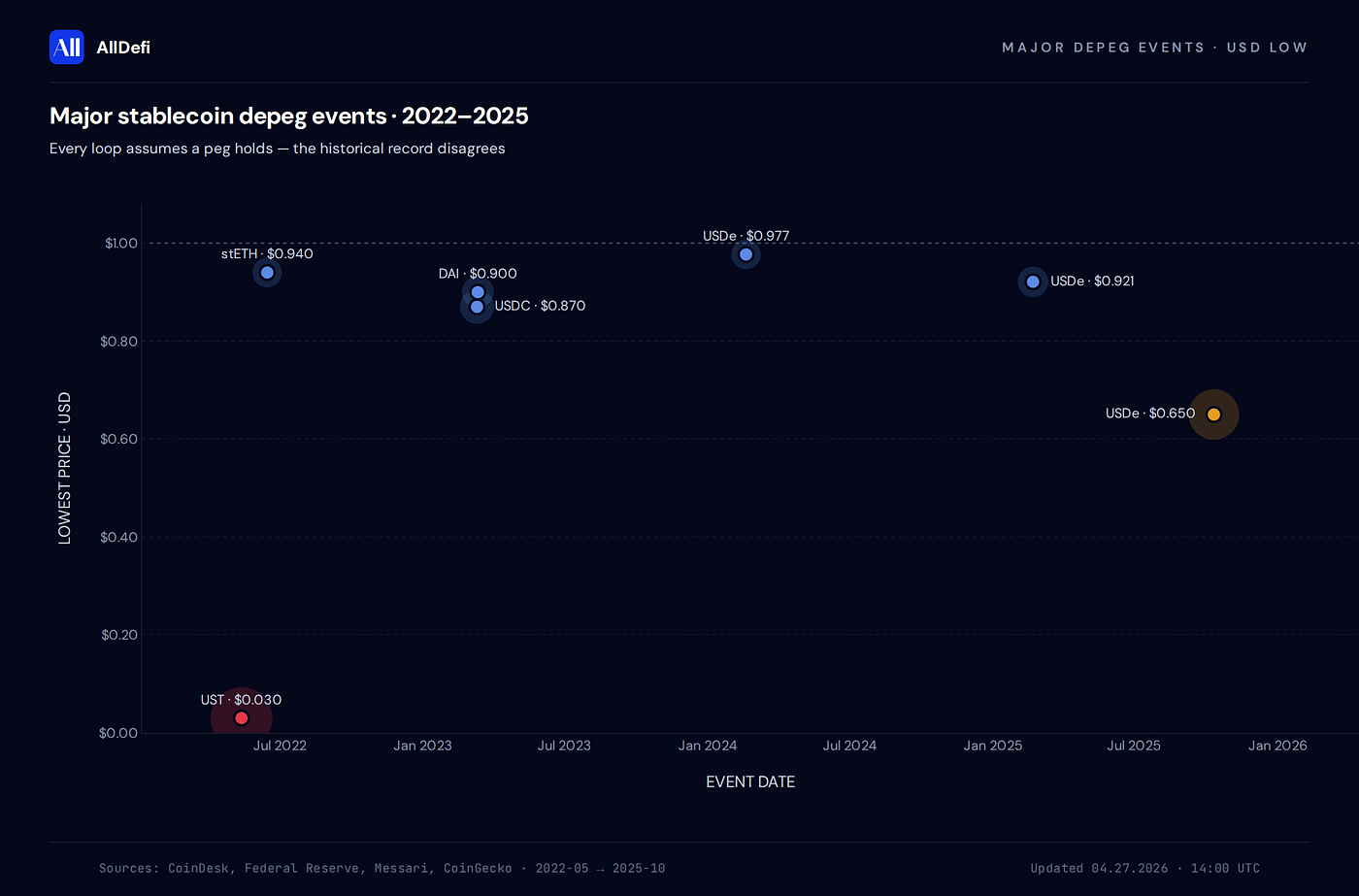

b. Stablecoin Depegs

Every stablecoin loop rests on one assumption: the two stablecoins stay 1:1 forever.

But a peg is a market state, not a protocol guarantee.

- USDe can depeg. If Ethena’s hedging mechanism comes under stress, market makers pull liquidity, or funding rates turn negative for extended periods, USDe can fall below $1. For a 10x loop, a drop to $0.95 means collateral value contracts 10% while debt stays priced at 1:1 — an instant liquidation trigger.

- USDT can depeg too. During the March 2023 SVB event, USDC briefly fell to $0.87; USDT itself has traded at premiums and discounts on several occasions. If your loop borrows USDT against another stablecoin, a USDT depeg in the opposite direction hits your position just as hard.

The damage from a stablecoin depeg is amplified by leverage. A 5% depeg is a non-event in spot trading. For a 10x loop, 5% equals 50% of equity.

These events tend to erupt overnight or on weekends — humans sleep; the chain doesn’t.

c. Liquidity Shortages

This is the most overlooked — and the most insidious — risk.

You might not be liquidated. The spread might not have inverted yet. But — when you want to exit, you can’t.

Two typical scenarios:

- The lending protocol runs out of USDT. You’re sitting on leveraged USDe deposits and USDT debt, and unwinding the loop requires repaying USDT first. When the entire market is trying to repay USDT at the same time, USDT borrow rates can spike past 30%. You’re stuck choosing between exiting at a loss or burning punitive interest while you wait.

- DEX depth on USDe / USDT dries up. Each round of unwinding requires swapping USDe back into USDT. Normally slippage is a few basis points. During stress, it can widen to 1–2%. On a 10x loop, slippage alone can eat a year of profit.

Looping can be exited in good conditions. In bad conditions, the exit itself becomes the cost.

How to unwind in batches, which route to take, how to allocate liquidity across chains — these questions change by the minute during a stress event.

d. Mass Liquidations (Liquidation Cascade)

Looping positions tend to be highly concentrated in a small number of strategies. Addresses running USDe/USDT loops on Aave look almost identical in structure.

That means when the first wave of positions gets liquidated, their collateral is dumped on DEXs. USDe gets pushed down. USDT borrow rates get pushed up. The next wave of positions hits the liquidation threshold. Chain reaction.

The 2022 stETH event, the UST collapse, multiple LRT depegs — all exhibit this cascade structure.

Your liquidation price is not set by your own leverage. It is set by the combined leverage of every participant in the market. This is the most counterintuitive — and most dangerous — property of looping.

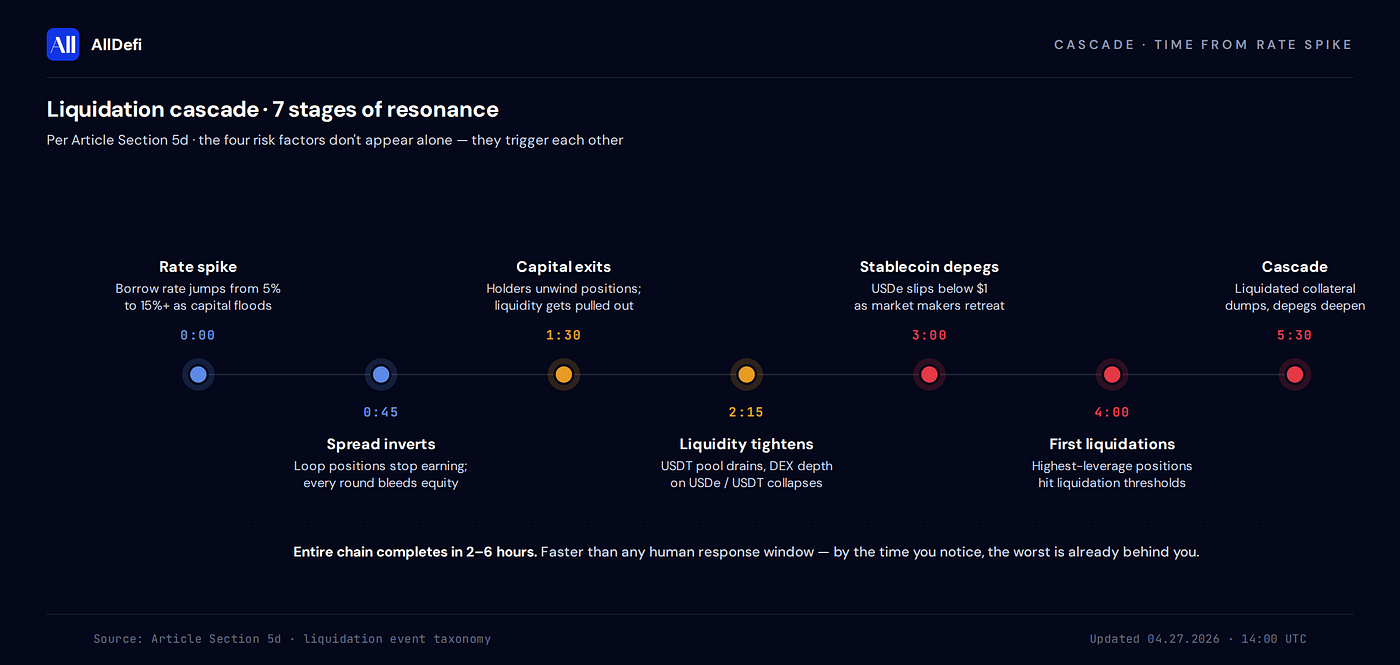

Resonance Between the Four Factors

These four rarely appear alone. They trigger each other:

Rate spike → some positions start losing money → capital tries to exit → liquidity tightens → stablecoin depegs briefly → first wave of liquidations → selling pressure worsens the depeg → liquidation cascade

Every major looping event in history leaves a footprint somewhere on this chain.

And the entire chain can complete within 2–6 hours.

6. The Structural Problem With Manual Looping

Stepping back from the mechanics, the fundamental problem with retail and small-fund looping becomes clear:

Returns are linear. Risks are discontinuous. Monitoring costs never stop.

To earn stable returns from looping over time, you need:

- 24/7 monitoring of borrow rates, DEX depth, and peg conditions across multiple chains

- Sub-second response to approaching liquidation thresholds, rate inversions, and liquidity deterioration

- Multi-chain routing, because the optimal execution environment for the same loop strategy often drifts between chains

- Exit path playbooks — knowing how to unwind in batches, which route to take, and what cost to accept during a stress event

- Disciplined scaling logic that isn’t swayed by market sentiment

None of these are things you can do just by “understanding DeFi.”

This is why the addresses that run looping sustainably on-chain are almost entirely market makers and quant teams with automated execution systems — not because they’re smarter, but because they’ve turned these capabilities into infrastructure.

For everyone else, these capabilities don’t exist. So the returns of looping, in the end, only flow to a small few.

7. What AllDefi Is Building

AllDefi is a Multi-chain Institutional Yield Layer. Our view is:

Looping is one of the few structurally clean sources of alpha in DeFi — but it should be handed to machines, not to retail.

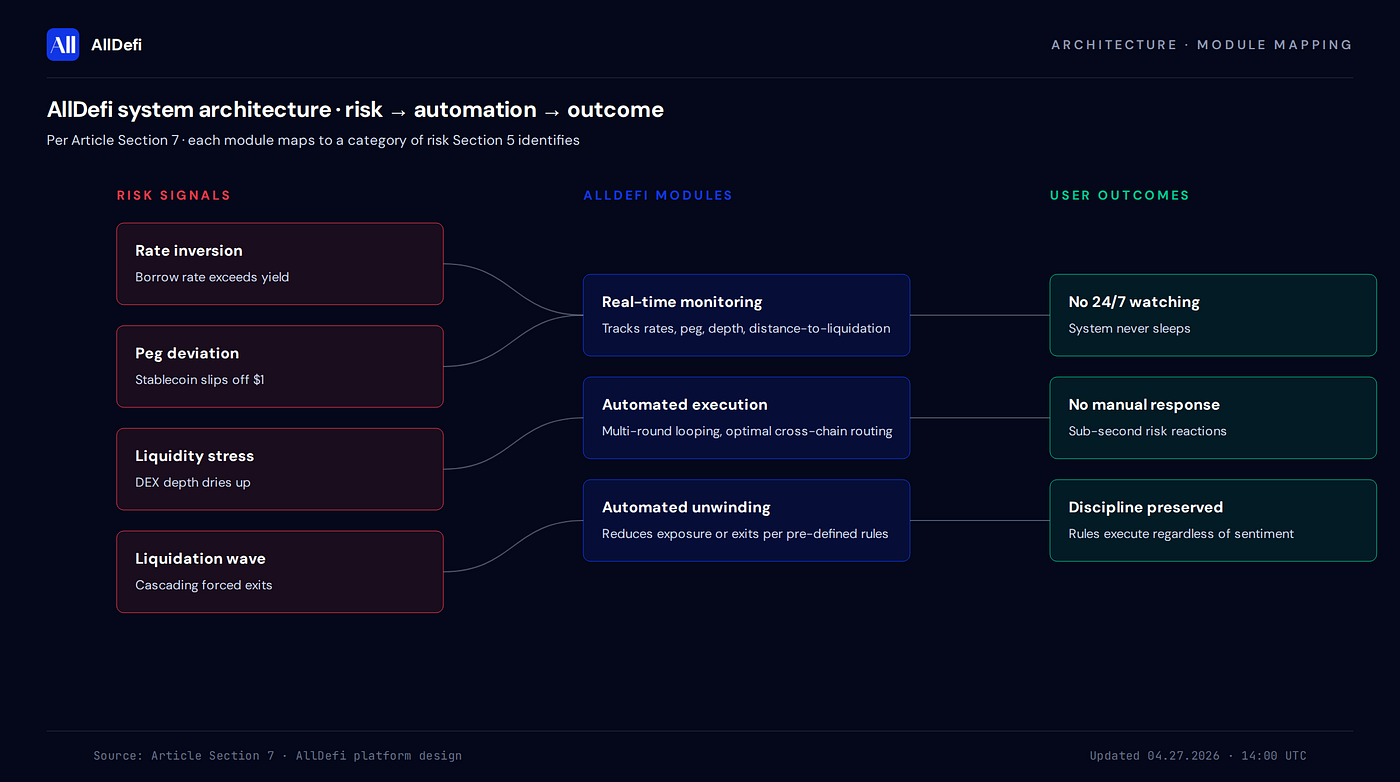

Based on that view, the system we’re building maps directly onto the four risk categories from Section 5:

- Automated looping execution — Executes multi-round lending and swapping according to strategy configuration, selecting the optimal path across chains. Users don’t need to understand every step, and they don’t need to operate anything by hand.

- Real-time risk monitoring — Continuously tracks borrow rates, deposit yields, peg conditions, DEX depth, and distance-to-liquidation. The moment any signal crosses a threshold, the system responds. It doesn’t depend on the user being awake.

- Automated unwinding and deleveraging — When rates invert, pegs deviate, or liquidity deteriorates, the system reduces exposure or exits entirely according to pre-defined rules. Users don’t sit passively waiting to be liquidated.

We believe the next stage of maturity in DeFi yield strategy doesn’t come from new strategies. It comes from the engineering depth between strategy and automated risk management.

Looping is just our first yield module.

Series Roadmap

This is Part 1 of the DeFi Yield Strategy Series. Upcoming pieces will go deeper on each risk factor in looping, and progressively unveil the design logic of AllDefi’s automated system:

- (2/N) Rate inversion: how many days it takes a loop to give back its profits

- (3/N) Tail risk of depeg: the conditions under which stablecoins, LSTs, and LRTs lose their pegs

- (4/N) The cost of exiting under liquidity stress: real-world slippage and borrow rates during crisis events

- (5/N) On-chain looping concentration: a backtest using Aave V3 mainnet data

- (6/N) From retail looping to automated looping: the AllDefi system architecture

AllDefi is a Multi-chain Institutional Yield Layer, delivering structured DeFi yield strategies to institutional capital — along with the automated risk infrastructure required to run them. This report is for research purposes only and does not constitute investment advice.