Canton’s $377M “Inflationary Loss” Is the Wrong Frame

A headline number is making the rounds: Canton is running on a $377 million inflationary loss.

The number may be useful as an annualized snapshot, but the framing is wrong.

Canton is not a company burning cash to keep a network alive. It is a protocol operating with a burn-mint equilibrium, where usage fees are burned and new Canton Coin is minted for participants that contribute to the network. Canton’s own FAQ describes this model as one where usage fees are burned, new coins are minted based on participation, and supply becomes responsive to demand and network usage.

That distinction matters.

If you simply look at a dashboard and say, “incentives are greater than fees burned, therefore Canton is losing money,” you are not really analyzing Canton’s tokenomics. You are flattening a dynamic monetary mechanism into a basic revenue-versus-expense spreadsheet.

What the $377M spread actually means

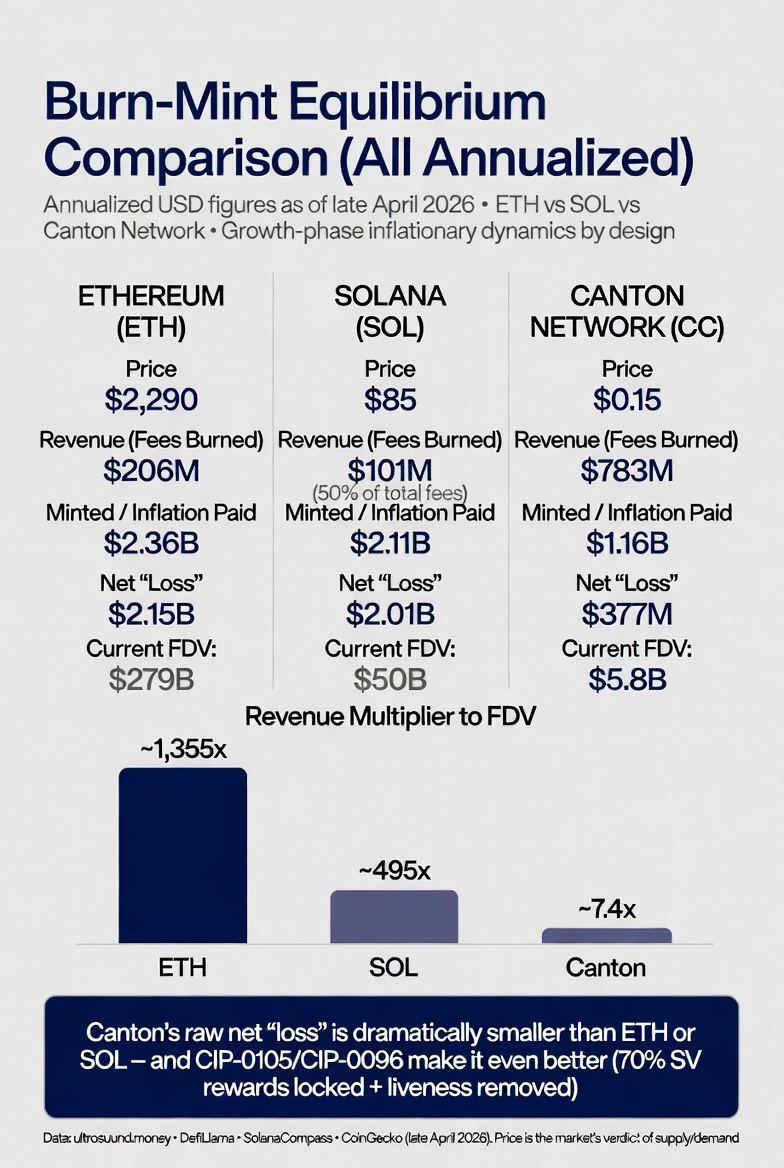

Using the numbers from the source post, Canton is currently around $1.16 billion in annualized minted rewards versus roughly $783 million in annualized burns, implying about $377 million in net annualized issuance.

That should not be ignored. Net issuance matters. Supply expansion matters.

But it should be described accurately: this is protocol-level net inflation, not an operating loss.

The better question is not whether Canton is inflationary in this exact snapshot. The better question is whether minted rewards are being used to bootstrap durable economic activity that eventually drives higher burns.

That is the point of the burn-mint equilibrium.

Canton fees are denominated in USD, paid in Canton Coin, and then burned. Minted rewards are distributed separately to validators, Super Validators, and application providers based on their contribution to network utility. The system is designed so that, over time, burns from actual usage can increasingly offset minted rewards.

Fees burned are a usage signal

Canton’s burns are not random. They are tied to paid network usage.

When participants use the Global Synchronizer to move assets, settle transactions, purchase traffic, or interact with Canton Coin, fees are paid and burned. Those burns are therefore a direct signal of economic activity on the network.

That does not mean every burned coin should be treated as perfect proof of high-quality institutional flow. But it does mean burns are connected to real network usage, not a generic accounting entry.

This is why the “loss” framing misses the point. Canton’s economics are designed to move between growth and maturity phases. In the growth phase, minted rewards can exceed burns as the network incentivizes participation. In the maturity phase, if usage expands meaningfully, burns can close the gap or exceed issuance.

Why incentives do not mean the same thing everywhere

A major mistake is treating all crypto incentives as identical.

On many networks, incentives are mostly understood as validator or staking rewards. Canton is different. Its reward structure is designed to evolve toward the participants generating the most utility.

Canton’s own tokenomics materials say that, in the current phase, applications are eligible for 62% of the reward pool, while Super Validator allocations have decreased to 20% until mid-2029. That is a deliberate shift away from pure infrastructure bootstrapping and toward applications, users, and productive network activity.

In other words, Canton is not simply paying people to stand up infrastructure forever.

The system is being pushed toward usage.

CIP-0096 tightened validator incentives

CIP-0096 is one of the most important changes in this discussion.

The proposal, titled “Removing Liveness Rewards from Validator Rewards Pool,” was approved to reduce the free-rider problem created by validators collecting rewards for liveness without otherwise adding meaningful utility to the network. It set a step-down schedule for validator liveness rewards, ending with the liveness reward cap going to zero on April 30.

That matters because liveness rewards had become a large passive component. CIP-0096 states that, over the reviewed 11/8–12/7 period, roughly 70% of validator rewards minted from the validator minting pool were associated with liveness rewards. The proposal’s rationale was to shift incentives toward active participation as on-chain use cases and activity grew.

So when critics treat Canton’s emissions as if nothing has changed, they are missing the direction of travel.

A large passive reward component has been explicitly reduced and removed.

CIP-0105 changes the supply conversation

CIP-0105 is the other major piece being overlooked.

The proposal introduced a Super Validator locking and long-term commitment framework. It does not mean every Super Validator reward is automatically and universally locked in every situation. The accurate version is more specific: Super Validators that want to earn forward Super Validator Weight must actively lock a defined percentage of their aggregate lifetime earned SV rewards. At the start of the framework, Tier 1 requires 70% locked to earn 100% forward weight.

That lock requirement includes both historical SV rewards and future SV rewards. CIP-0105 also says only actively locked Canton Coin counts toward the SV weighting algorithm, and unlocks vest gradually over time rather than becoming liquid immediately.

This materially changes how emissions should be discussed.

Since the current reward structure lists Super Validators at 20% of the reward pool, a Tier 1 lock of 70% on that allocation implies that up to 14% of gross future emissions could be economically restricted through SV locking for Super Validators maintaining full forward weight.

That is not the same as saying “all emissions are liquid incentives.”

It is also not the same as saying “70% of all future Canton emissions are locked.”

The precise point is this: CIP-0105 reduces the immediately liquid profile of Super Validator rewards for participants seeking full forward weight.

That is a meaningful supply-side distinction.

Price is an input, not a magic fix

There is also a more subtle point around price.

Because Canton fees are USD-denominated but paid in Canton Coin, a lower CC price does not necessarily make network usage cheaper in USD terms. Instead, it can mean more CC must be burned for the same dollar-denominated activity. A higher CC price can mean fewer CC are burned for the same dollar-denominated activity.

So price is not a simple “usage gets cheaper, therefore usage rises” mechanism.

The more accurate way to frame it is this: price affects how many CC are burned for a given level of dollar-denominated network usage, while actual adoption determines the size of the fee base. Over time, the burn-mint equilibrium is designed to respond to both network activity and token supply dynamics.

That is very different from a fixed subsidy model.

The current state is not the end state

The current net inflation figure is not meaningless.

But it is also not the end state of Canton’s design.

Canton is still in a scaling phase. The protocol is using emissions to attract participants, reward applications, support infrastructure, and grow real economic activity on the network. At the same time, its governance process is already tightening incentives: CIP-0096 removes pure liveness rewards, while CIP-0105 creates a stronger long-term alignment mechanism for Super Validators.

That is the real story.

The headline should not be “Canton is losing $377 million.”

A more accurate framing is:

Canton is currently net inflationary on an annualized basis, but that inflation is part of a burn-mint design intended to bootstrap usage, reward productive activity, and eventually move toward equilibrium as network activity scales.

The number matters.

But the interpretation matters more.

Canton’s tokenomics are not trying to hide the spread between minted rewards and burned fees. They are designed around it. The system is meant to expand during growth, tighten as usage rises, and reward participants based on real contribution rather than speculation alone.

The current net inflation is not the whole game.

The transition from bootstrapped growth to utility-driven equilibrium is the game.