In recent weeks, the @CantonNetwork has sparked intense discussion across the crypto & institutional finance communities. Amidst a wave of strong opinions & technical critiques, I felt compelled to share a more nuanced perspective, one grounded in both my experience building at @fairmint and my role on the Board of Directors of the @CantonFdn , where I was elected to represent the General Members.

I. You Can Lead a Horse to Water, but You Cannot Make It Drink

For the better part of a decade, the blockchain industry made a pitch to capital markets that capital markets did not ask for.

‘Your infrastructure is obsolete, your intermediaries are rent-seekers, your settlement cycles are an embarrassment, and if you would just put everything on Ethereum, the problem goes away. Trust the math. Trust the code. Trust the network.’

The pitch was not entirely wrong. Settlement cycles are an embarrassment. Intermediary stacks do extract rent at every layer. The post-trade infrastructure that processes trillions of dollars in global securities transactions still runs on architectures from an era when moving a stock certificate meant moving a physical piece of paper between vaults. The 2021 meme stock episode demonstrated, in public, that the plumbing behind US equity markets is held together with duct tape and two-day settlement windows that exist because of organizational inertia, not just technical constraint.

But the pitch failed. Not because it was wrong about the problem. Because it was wrong about the audience.

The people building decentralized finance protocols understood smart contracts, MEV, and AMM curve design. They did not understand prime brokerage agreements, the role of the DTCC as a central counterparty, why tri-party repo exists, what Reg SCI actually requires, how a transfer agent processes a corporate action, or why a custody bank employs 40,000 people. They assumed that the complexity of traditional financial infrastructure was the result of institutional laziness or regulatory capture. Some of it is. Much of it is the accumulated response to real operational requirements that crypto protocols have never had to face: contested ownership, court orders, estate administration, regulatory examinations, fiduciary duties owed to pension funds managing the retirement savings of millions of people.Crypto built an extraordinary sandbox - smart contracts, composability, AMMs, lending protocols, on-chain governance, programmable settlement - and then tried to convince institutions managing hundreds of trillions in assets to abandon their existing infrastructure and join the sandbox. The institutions said no. Not because they didn't understand blockchain, but because they understood their own obligations better than the crypto people pitching them.Asking institutions to abandon their existing infrastructure produced enormous innovation and enormous frustration. It also created a false binary that has poisoned the conversation ever since: permissionless or permissioned, crypto or TradFi. As if the $500 trillion in global financial assets and the $3 trillion crypto market are competing for the same philosophical territory rather than occupying radically different points on the same spectrum of financial infrastructure.

II. What Each Side Built, and What Each Side Missed

The first decade of blockchain experimentation produced genuine infrastructure primitives.

- Programmable settlement: encoding the terms of a financial transaction into software that self-executes in twelve seconds what a traditional settlement process does in two days across six intermediaries.

- Composability: any protocol building on any other protocol without permission, without an API agreement, without a business development negotiation — an architectural property that changes the economics of financial product development and that traditional finance has nothing remotely equivalent to.

- Self-custody: eliminating an entire category of counterparty risk, as the FTX collapse demonstrated with brutal clarity.

- Transparent settlement finality: publicly verifiable, irreversible, final — eliminating the entire category of post-trade disputes that currently occupy thousands of operations professionals at every major bank.

- Automated market making (AMM): demonstrating that continuous liquidity provision does not require an order book, a market maker with a prime brokerage relationship, or exchange membership — with direct implications for asset classes that are currently illiquid because the traditional market-making infrastructure is too expensive to deploy.

These are not toys. These are infrastructure primitives that solve real problems in capital markets.But the institutions that declined crypto's pitch did not do so out of ignorance. They did so because the pitch ignored their actual constraint set. A hedge fund cannot have its positions visible on a public blockchain. A bank's repo book cannot be queryable by its competitors. Securities regulation - KYC/AML, accredited investor verification, transfer restrictions under Regulation D & S, Rule 144 holding periods, FATCA - is not optional and not simple. A custodian bank with fiduciary obligations cannot delegate them to a smart contract. A broker-dealer cannot route client orders through a protocol it does not control and cannot audit. A transfer agent registered under Section 17A of the Exchange Act cannot outsource its record-keeping to a system where no one is legally accountable.

These are not bureaucratic preferences. They are legal requirements that attach to regulated entities. And they are the requirements that 'killed' every previous generation of "enterprise blockchain."

III. Canton: The Infrastructure Nobody Loves and Everybody Needs

Canton was built specifically to meet institutional requirements: need-to-know privacy, institutional control points, compliance integration, and an operating model aligned with existing regulatory obligations.

The crypto community's reaction has been almost uniformly hostile. The criticisms are real and in some cases, as @ShaulKfir commented over the week-end, technically valid. Swen Werner 's analysis of synthetic atomicity, cross-firm deployment overhead, and the independent verifiability problem all identify genuine architectural limitations. @lex_node 's "Intermediary Cosplay" critique argues that Canton re-intermediates at the infrastructure layer. Alex Gluchowski contends that Canton's integrity model relies on trusted operators rather than cryptographic verification.

I take these comments seriously, and I say that as someone with skin in the game. I sit on the board of the Canton Foundation, Fairmint deploys cap tables of its customers on Canton after working for years on Ethereum, Optimism, and Base.

But the criticism misses something fundamental about what Canton represents, not as a technology, but as a market event.

Canton has accomplished what no public blockchain has yet accomplished in capital markets: it has persuaded major financial institutions to move beyond study and pilot rhetoric into live institutional deployment. DTCC has committed to bringing a subset of DTC-custodied U.S. Treasury securities onto Canton, starting with an MVP in a controlled production environment. Broadridge's DLR platform has reported $280 billion in average daily processed trade volumes and more than $15 trillion in monthly repo notional settled. Visa has joined Canton as the first major global payments company selected to serve as a Super Validator, as announced during DAS NYC 2026 last week. Goldman Sachs's GS DAP is natively on the network.Canton is increasingly presenting itself as a public, permissionless network at the base layer, while still delivering the privacy, selective disclosure, and institutional control points that regulated institutions require at the application layer. The crypto community can dismiss this as "permissioned blockchain theater."

None of that changes the fact that major financial institutions are moving real workflows, real assets, and real transaction volume onto Canton-based infrastructure. And that fact creates what I believe is the largest infrastructure opportunity in digital assets.

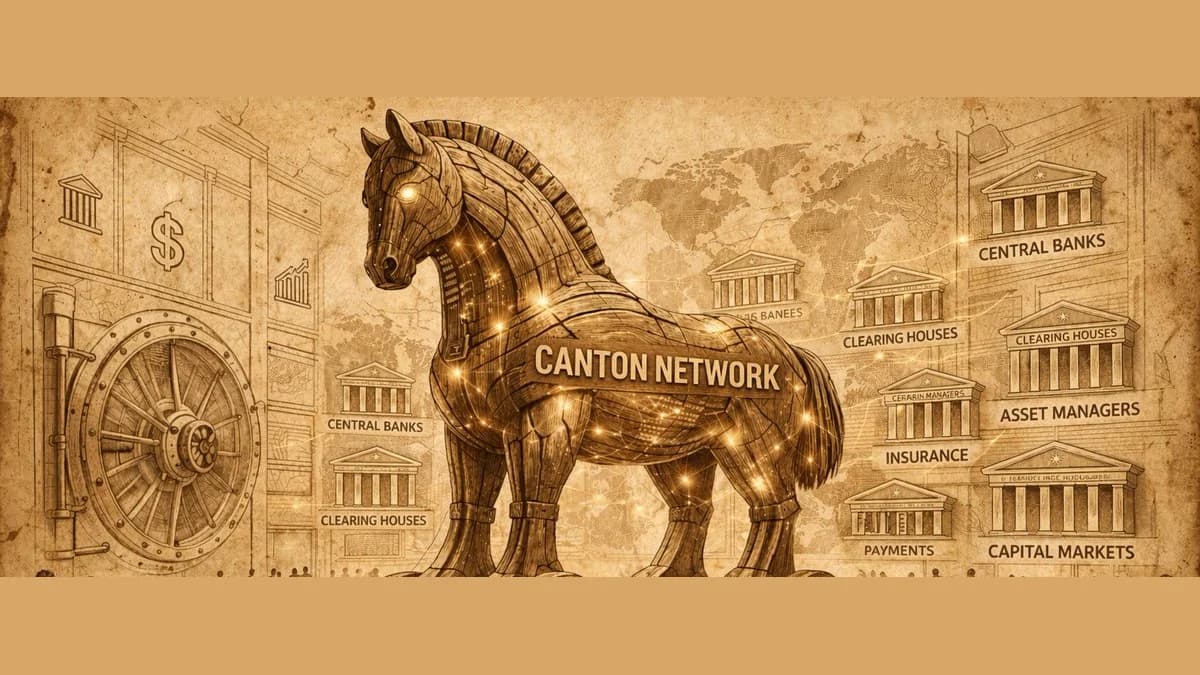

IV. The Trojan Horse Thesis

Here is the argument that neither the permissionless camp nor the Canton camp is making, because each side is arguing from inside its own worldview.

Canton is not the enemy of permissionless finance. Canton is the on-ramp.

The moment institutional-grade financial assets settle on digital infrastructure - any digital infrastructure - the composability question becomes real. Not as a theoretical possibility. As a market demand.

When trillions in Treasuries, corporate bonds, and equity securities are represented as digital assets on Canton's settlement layer, those assets exist in a programmable environment. They have digital representations. They can, in principle, be referenced, collateralized, traded, and composed with other digital assets - if the infrastructure exists to bridge them.

Canton is designed as a network of interoperable synchronization domains. Its Global Synchronizer enables atomic transactions across different Canton domains. Canton's architecture suggests a path toward interoperability beyond purely Canton-native environments, provided the right connectors, trust assumptions, and control frameworks exist. The same interoperability logic that connects Canton domains could, in principle, be extended through bridges or connectors to public chains, subject to the right trust assumptions, controls, and technical design.

This is the Trojan Horse.

The highest-quality collateral in the global financial system - tokenized Treasuries, repo positions, corporate bonds - settling on Canton and becoming bridgeable to permissionless execution environments. Institutional settlement provides the assets. Permissionless rails provide the composability, the liquidity, the 24/7 markets, the automated market making.And it goes beyond composability. Canton's institutional participants - DTCC, Broadridge, Goldman Sachs, Visa, the major custodian banks - collectively have relationships with virtually every institutional investor, pension fund, sovereign wealth fund, insurance company, and asset manager on the planet. They are the distribution infrastructure of global capital markets. Any ecosystem that can interoperate with Canton-settled assets positions itself closer to that distribution. Not by convincing Goldman Sachs to "adopt Ethereum." By making Ethereum-based protocols useful for assets that Goldman Sachs is already settling on Canton.

This inverts the go-to-market problem that has plagued crypto adoption for a decade. Instead of asking institutions to come to crypto, you bring crypto's capabilities to where institutions already are.

V. The Layered Thesis

This is not a compromise. It is an architecture.The settlement layer does not need to be permissionless. The composability layer does. These are different functions with different requirements, and they can, and should, be separated.

The settlement layer needs privacy, institutional control, regulatory compliance, and operational resilience. Canton provides this. The composability layer needs openness, permissionless access, programmability, and transparent execution. Public chains provide this.

The bridge between them is where the value is created.

The same pattern has played out in every layer of internet infrastructure. TCP/IP is a permissionless protocol. The fiber optic networks it runs on are owned by regulated telecommunications companies. The web is open. The data centers that serve it are operated by a handful of hyperscalers with compliance obligations, government contracts, and operational requirements that no decentralized network could satisfy. The value of the internet is not in the data centers or in the protocols alone. It is in the composability between layers with different trust models.

Financial infrastructure is heading to the same place. The question is not whether the future is permissioned or permissionless. The future is layered.

VI. The Challenge: the Open Standard Imperative

None of this works without a shared language. Interoperability between Canton domains and public chain ecosystems requires a common representation layer: a standard for how ownership records, transfer restrictions, corporate actions, and compliance metadata are encoded, regardless of which settlement infrastructure the asset lives on.

The interoperability standard will look different for each asset class. Fixed income, derivatives, and structured products will each require their own representation layers, their own data schemas, their own compliance metadata formats. But the pattern is the same: a shared, open standard that any participant can read and write to, regardless of which settlement rail the asset lives on.

In equity markets - the layer I know best, and the one Fairmint has spent years building for - that shared language is exactly what open standards such as the Open Cap Table Format (OCF) were created to address. OCF emerged from the Open Cap Table Coalition - a broad effort spanning law firms (Cooley, Gunderson, Orrick, Latham, Wilson Sonsini, among others), equity platforms, and ecosystem participants - to make cap table data portable, interoperable, and machine-readable. Fairmint's Open Cap Table Protocol (OCP) extends that logic onchain: an open-source standard deployed on Ethereum (Optimism, Base), and Canton, so that any transfer agent, broker-dealer, or issuer can read and write to the same format. Not a proprietary platform. Not locked to a single chain. Deployable wherever assets need to move.

The 1969 parallel matters here. When North American Rockwell analyzed the paperwork crisis for the American Stock Exchange, they proposed two paths: centralize everything through one hub (which became The Depository Trust & Clearing Corporation (DTCC) ), or build a distributed network of transfer agent depositories linked through a common communications standard. The industry chose centralization because the technology for the distributed path didn't exist at the time.

Both exist now. Distributed ledger technology provides the network. OCP provides the shared language. What Rockwell described in 1969 - a distributed network of transfer agents acting as both custodians and source of truth for ownership - is what we are building at Fairmint, fifty-seven years later, with the tooling and the open standard that finally match the vision.

VII. A Constructive Truth for Both Sides

For the crypto maximalists: Canton is not going away. The institutions that run global financial infrastructure chose it for reasons that have nothing to do with ideology and everything to do with real operational, privacy, and regulatory requirements. Dismissing it as “blockchain theater” is emotionally satisfying but strategically shortsighted. The highest-quality collateral and settlement flows are heading there. The real question is whether we build the infrastructure to connect to those assets, or remain a sidecar to a system that doesn’t need our permission to exist.

For the TradFi camp: a settlement network optimized for institutional privacy and control delivers immense value, but its full potential is only realized when those settled assets become truly composable. Moving assets from one intermediary database into another DAML-based workflow improves efficiency, yet stops short of unlocking the exponential innovation that tokenization promises.

The Super Validators & leaders at @digitalasset (@YuvalRooz Rooz @ShaulKfir @wesarn_real Bernhard Elsner @waynecollier111 ), @DRW / @CumberlandSays (@drwconvexity @Chris_Zuehlke ), at the Canton Foundation ( @viv_diwakar @MlvsBznz ), @CantonStrategic (@MarkWendlandCSH @Mark Toomey) , @FiveNorthHQ (@bc1pxxx ) , at Liberty City Ventures (James Lang) , at Broadridge ( German Soto), at Tradeweb (Justin Peterson), @7RIDGE1 (@veronicaaugusts ), at MPCH ( Kinga B.) & all the board members of the Canton Foundation (@Obsidian @RyanTrinkle , @IntellectEU ,@BitwavePlatform , LTP, SBI, BNY, BNP, HSBC, @trize_io with co-chairs @EuroclearGroup ( Jørgen Ouaknine ) & @The_DTCC ( Johnna Powell ) clearly understand this.

That’s why, on top of onboarding most of the financial institutions, we’re already seeing meaningful progress on the Canton Network: the Global Synchronizer enabling atomic cross-domain transactions, the subdomains, the ongoing development toward broader execution compatibility, and the active efforts (such as the recent LayerZero integration) to enable secure and compliant connectivity with public execution environments.

A settlement network that cannot interoperate with permissionless composability layers would risk becoming a highly sophisticated, yet ultimately isolated, digital filing cabinet. The true leap forward happens when tokenized Treasuries, repo positions, and institutional assets on Canton can be used as collateral, traded, or programmed atomically alongside DeFi primitives on open rails. That composability lives also on permissionless infrastructure. Build strong privacy-preserving settlement and open, well-designed connectors, and you don’t just get a better database. You get the foundational settlement layer of the next financial system. There is no more permissioned vs. permissionless.

Conclusion

"This is the end of the beginning" SEC Chair Atkins, Blockworks DAS NYC 2026

The onchain opportunity is not about choosing sides in a decade-old debate. It is about building the right architecture. A future financial system where institutions have the privacy, control, and regulatory compliance they need, while the most powerful innovations in composability, liquidity, and 24/7 markets continue to flourish on permissionless rails.

This requires different trust models for different layers: trusted settlement infrastructure where it matters most, open and permissionless execution where innovation moves fastest, and open standards + secure connectors that bind them together.

That is the layered thesis.

And that is exactly our vision while building at Fairmint: the open protocols and interoperability standards (such as the Open Cap Table Protocol) that turn onchain institutional assets into truly programmable, composable instruments, without forcing institutions to abandon the infrastructure they actually need.

The Trojan Horse is already inside the gates & it's a massive victory for innovators. Now the real work begins.

Builders, are you ready?