Private markets have a new problem.

For years, the issue was access.

The best private companies were locked behind relationship networks, fund allocations, family offices, SPVs, and minimum tickets most investors could never meet.

That problem still exists.

But now a second problem is emerging. The first wave of products trying to open pre-IPO exposure often prices that exposure badly.

Not slightly badly, but structurally badly.

People want exposure to the next generation of private technology giants, and that demand is rational because the private market has become too large to ignore.

However, most existing pre-IPO access products are static wrappers around scarce assets. They acquire a limited amount of underlying exposure, issue a limited amount of product, and then let secondary-market demand do the rest.

When demand spikes, the product cannot easily create new supply backed by newly acquired shares. So the price rises above the value of what the product actually represents.

The premium created as a result is a scarcity tax.

Access is not the same as fair pricing

A private company can be priced fairly, and a product giving exposure to that company allows it to be priced very differently.

That gap is the problem.

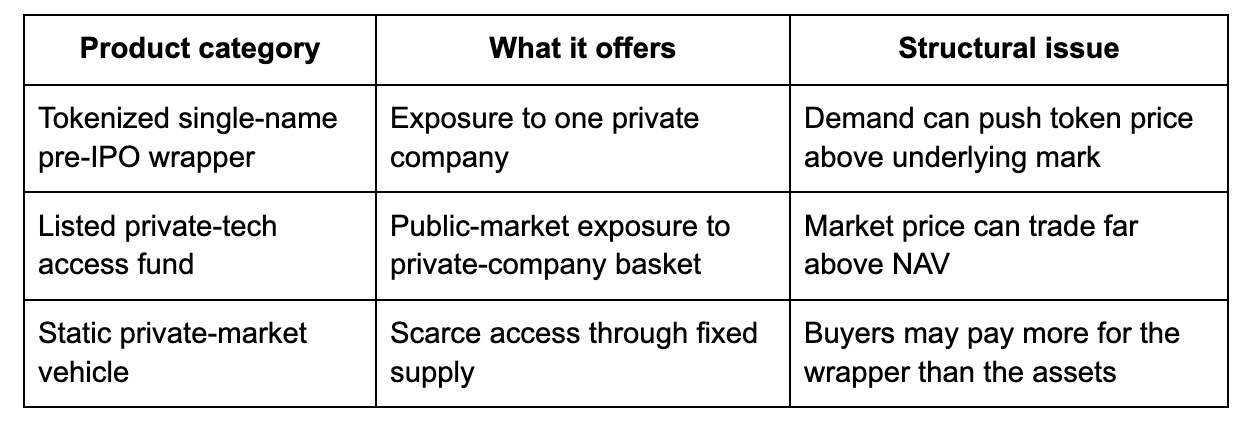

Across tokenized single-name pre-IPO products, listed private-tech funds, and static access vehicles, the same pattern keeps appearing:

- The product gives people access.

- The market bids that access above the value of the underlying exposure.

At that point, the buyer is not just buying the private company. They are buying the private company plus a wrapper premium.

That distinction matters.

If you pay 40%, 80%, 200%, or more above the underlying mark or NAV, the company has to appreciate just for you to get back to fair value.

The scarcity premium

When a product acquires exposure to a company like Anthropic, it issues a token or share representing that exposure.

Then demand comes in and more buyers want the product.

But the product cannot immediately acquire more underlying shares, expand its balance sheet, and issue more fully backed units.

So the market does the only thing it can do - it bids up the wrapper.

Not necessarily because the private company itself became more valuable overnight, but because access became scarce.

That is the crux of the scarcity premium problem.

And it creates a very different trade from what most investors think they are buying.

They think they are buying pre-IPO exposure.

In reality, they are buying:

- Pre-IPO exposure

- Plus wrapper scarcity

- Plus the risk that the premium later collapses

This creates a structural pricing problem, which then leads to a likely failure loop:

- Demand enters

- Supply cannot expand

- Wrapper price rises

- Premium to NAV expands

- Buyers overpay for access

- Repeat

This is not just an on-chain problem

This issue is not limited to tokenized products.

It also exists in off-chain markets.

Closed-end funds and static listed vehicles can trade at premiums or discounts to the value of their underlying assets because their share price is set in the market, while their NAV is calculated separately. That is a known structural feature of closed-end products.

The same dynamic now appears in pre-IPO access.

When the underlying assets are difficult to source, hard to value, and impossible for most investors to buy directly, the wrapper becomes the only liquid way in.

Demand concentrates in the wrapper, and if supply cannot flex, price detaches from value.

Investors finally get access to private markets, but they’re likely paying a massive tax to get there.

Crypto already learned this lesson

Bitcoin went through a similar evolution, and can be viewed as a similar analogy.

Before spot Bitcoin ETFs, early Bitcoin trust products gave investors a way to access Bitcoin through traditional brokerage accounts.

But structures were primitive.

Shares could trade above or below the value of the Bitcoin held by the trust because the product did not have the same open-ended creation and redemption mechanism as an ETF. Grayscale’s current ETF materials still note the basic reality that shares trade at market price rather than NAV and may trade at a premium or discount.

The ETF model improved this by making supply more adaptive.

ETF shares can be created or redeemed in response to market demand. Schwab describes this open-ended creation/redemption structure as allowing ETF shares to be added or subtracted to balance supply and demand while staying grounded in the value of the assets held by the fund. Vanguard similarly explains that creations and redemptions help keep ETF market prices in line with fair value and limit severe premiums and discounts.

The early trust model provided access, and the ETF model improved pricing.

Private markets are now at the same point.

The first wave of pre-IPO products provided access, and the next wave needs better pricing architecture.

Static products break under dynamic demand

The first generation of pre-IPO access products mostly shares the same limitation of being too static.

They acquire some exposure and wrap it. Then they list it, tokenize it, or make it tradeable. The market trades around a fixed or semi-fixed pool of underlying assets.

That can work when demand is calm, but it breaks when demand surges.

If thousands of new buyers want exposure to a private AI lab, space company, payments network, or infrastructure giant, but the product cannot efficiently source more underlying exposure and issue more backed units, the result is obvious:

- The wrapper price rises

- The premium expands.

- The product becomes more expensive than the asset it is supposed to represent.

At that point, the product is no longer simply providing exposure to a private company, but asking investors to speculate on the premium of the access wrapper itself.

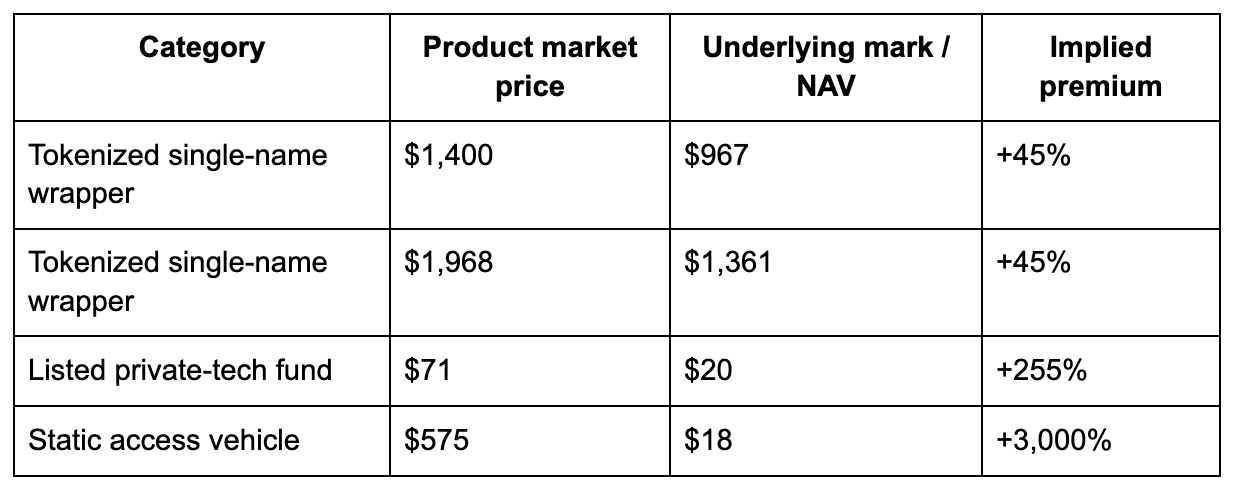

The table below is an example of how that looks.

The Hecto Approach

At Hecto, we’re building a model to solve that problem.

Not a static wrapper around scarce exposure.

Not a single name product where demand can overwhelm supply.

Not a tokenized version of the same old bottleneck.

The goal is a more adaptive pre-IPO index structure. One where demand, issuance, underlying acquisition, and NAV alignment can work together.

In the Hecto model, private shares are sourced through platforms, SPVs, or direct routes. SPVs are the preferred route for larger tickets, and our model focuses on leveraging a network of GPs, UHNWIs, family offices, and banks to access allocations that are typically unavailable to retail investors.

Those shares can then be placed into an SPV, tokenized, held through regulated custody infrastructure, and represented through receipt tokens on Canton.

But the important piece is the flywheel. When demand creates a premium to NAV, institutions can arbitrage that premium by minting.

- Minting increases supply.

- Fresh capital can be deployed into additional underlying exposure.

- The expanded supply helps compress the premium.

- The market becomes less dependent on scarcity and more anchored to backing.

That is the missing piece in current pricing architecture.

A healthy pre-IPO market does not just need a token, it needs a mechanism that lets supply respond when demand arrives.

The private market is becoming too large, too important, and too delayed from public markets to remain a relationship-only asset class.

It deserves a model that looks more like modern ETF infrastructure than a static trust.

It should be diversified, have transparent NAV logic, have flexible issuance, and allow new demand to translate into new backing instead of a higher premium.

What you get is not a bet on one name, but an allocation to a thesis that the world’s private giants will continue to create most of their value while private.