For most of crypto history, tokens were treated as the final product.

Issue the asset, build the community, list the token, add liquidity, then wait for the market to decide whether the project was infrastructure, speculation, entertainment, or an unusually expensive group chat.

That era has not ended, and it will continue to exist. But its center of gravity has shifted.

The market is moving from tokens as isolated instruments toward tokenised assets: stocks, treasuries, RWAs, structured yield, and vault strategies connected to existing economic activity. Major venues are following the same migration. Trading interest is no longer confined to the long tail of altcoins. Increasingly, capital is looking for assets with recognizable yield, collateral value, settlement advantage, or balance-sheet utility.

This does not mean the crypto market has disappeared. Capital rarely disappears. It reprices, rotates, and becomes less forgiving.

The market has upgraded.

From Narrative to Efficiency

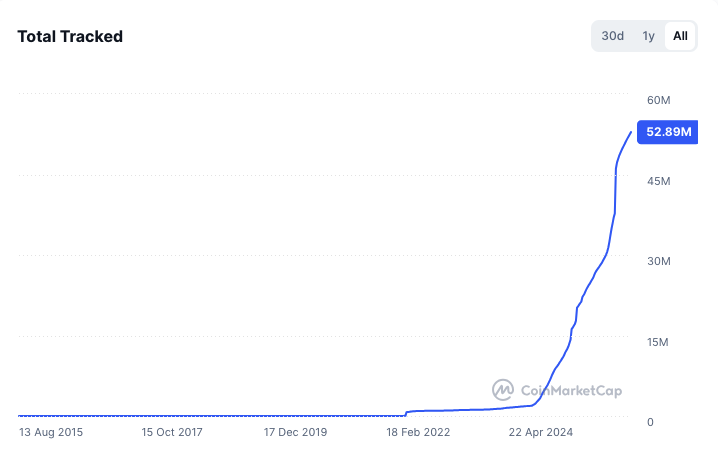

According to CoinMarketCap data observed across token listings, narrative-driven issuance accelerated sharply from Q4 2024 onward, 96.22% of all tokens tracked was created in the past 18 months. The number is cruel enough to make the point without theatre: a vast majority of listed tokens now compete for a shrinking share of durable attention, liquidity, and market capitalization.

Coinmarketcap Number of Cryptocurrencies Tracked H1 2026

How many still occupy meaningful mindshare today?

This reality does not make tokens irrelevant. It makes the purpose of tokenization more demanding.

A tokenised instrument must do more than exist on-chain. It should settle faster, move more efficiently, distribute yield more cleanly, support better collateral mobility, or improve capital access for a business that already has economic activity.

This is the quieter but more durable version of the on-chain finance thesis. It is less theatrical than a new retail meta and less sentimental than another “future of finance” panel. It asks a more useful question: does the system make existing financial activity more efficient?

That is where Canton’s position becomes interesting.

In a recent interview, Digital Asset co-founder @YuvalRooz made a point that cuts through much of the usual crypto theatre: traditional finance will always require credible middlemen. The business opportunity is not to pretend intermediation disappears. It is to make trusted intermediaries more efficient, more interoperable, and less constrained by slow settlement, fragmented liquidity, and inefficient treasury movement.

(This is the interview link: https://www.youtube.com/watch?v=P9_Kh7FRQlw)

That view is not anti-crypto. It is economically honest.

Financial markets already have demand. SMEs already need working capital. Insurers already manage risk. Asset managers already search for yield. Treasuries already optimize liquidity. Institutions already rely on trusted parties.

The opportunity is not to invent demand from a narrative cycle. It is to improve the infrastructure around demand that already exists.

Where Lending Fits

EQ Market is approaching mainnet with this shift in mind.

The first release is intentionally clear: $CC and $USDCx supply-and-borrow markets. Users will be able to supply assets, borrow against collateral, and begin forming the first usable credit circuit for Canton-native DeFi.

It is the entry point of our work.

A lending market gives tokenised assets a second life beyond issuance and transfer. It allows an asset to become collateral, support borrowing, generate yield for suppliers, and produce a reference rate that other applications can build around.

In mature DeFi ecosystems, lending became foundational not because it was glamorous, but because it provided a business model for the rest of the stack: collateral in, liquidity out, risk priced in between.

That model becomes even more important in the RWA context.

Tokenization without financing is mostly improved record-keeping. Useful, yes. Complete, no.

We are building toward a future where tokenised assets can support credit markets: invoices, receivables, insurance-linked assets, treasury instruments, and other cash-flow-based instruments financed through controlled, permission-aware lending environments.

This is the direction we are preparing for.

Beyond the Mainnet Launch

RWAs are not generic tokens with a different logo.

They may come with issuer requirements, visibility constraints, transfer rules, legal wrappers, counterparty obligations, or asset-specific risk terms. A serious lending layer should not flatten those realities into one anonymous pool and hope the footnotes behave.

Whitelisted markets give the protocol room to treat different assets differently.

SME invoice financing is not the same as treasury collateral. Insurance-linked exposure is not the same as stablecoin liquidity. Receivables are not the same as volatile native assets. Each market needs its own risk logic, participants, permissions, and liquidity assumptions.

Our team has been preparing the infrastructure for collateralised lending use cases that have been discussed across the industry for years but rarely brought close to functional deployment.

This demand is not theoretical.

EQ Market has been working with established entities offline and off-chain, where the value proposition is practical: improve capital efficiency, create additional yield opportunities, and unlock financing channels around revenue streams that already exist.

These industries did not need Canton, or us, to operate.

They were already operating.

That is precisely why the opportunity is real. The role of infrastructure is not to make itself the main character. It is to bring a better instrument to the table: faster settlement, cleaner collateral movement, more efficient credit access, and a yield layer built on top of existing economic activity.

The crypto market did not disappear.

It became more selective, more collateral-aware, and more interested in assets that can do something.

Our answer is credit.

Not as a slogan.

As infrastructure.