Confidential credit is onchain lending infrastructure designed for institutions: structured visibility instead of full transparency, controlled participation instead of open access, and segmented risk instead of shared pools. It is the credit layer institutional finance has been waiting for, and Canton is the rail built to support it.

Public DeFi proved that lending can work onchain. It did not prove that all lending should work the same way.

Institutions operate under constraints around disclosure, counterparty exposure, and operational control that transparent by default markets were never designed to accommodate. Confidential credit is infrastructure built for that gap.

At its core, confidential credit is about bringing credit onchain without forcing institutional users into an environment where transparency becomes an operational liability. It is not a rejection of DeFi, and it is not an argument against open markets. It is a recognition that some forms of finance require infrastructure that preserves privacy, supports controlled participation, and reflects how regulated financial actors actually use capital.

Why Credit Matters In The First Place

Every mature financial system consolidates around credit markets because credit makes capital more productive.

It allows assets to serve as collateral instead of sitting idle. It lets market participants access liquidity without exiting positions. It helps treasuries and balance sheets work harder. And it allows markets to scale beyond the limits of immediate cash ownership.

The same logic applies onchain. The question is not whether lending can exist on blockchain infrastructure. It clearly can. The more important question is what kind of lending infrastructure is required when the users are not anonymous traders optimizing for openness, but institutions operating under mandates, controls, and competitive constraints.

That is why credit remains the missing primitive for institutional onchain finance. Open lending exists. Institution ready credit infrastructure is still being built.

Why Traditional Credit Markets Depend on Discretion

In serious financial markets, discretion is not cosmetic. It is part of market structure.

A credit relationship can reveal a great deal: liquidity needs, changes in positioning, funding pressure, portfolio adjustments, or views on risk. If every borrowing action, collateral change, and liquidation signal were exposed by default, participants would leak information every time they managed their balance sheet.

That is one reason real credit markets do not function as fully transparent glass boxes. Visibility is controlled. Access is bounded. Sensitive information is shared on a need to know basis.

For institutions, that is not simply a preference. It is part of how markets remain usable. Markets work more effectively when risk is routed to the relevant parties rather than broadcast to everyone at once.

Why Public Chain Lending Is Not Confidential Credit

Public DeFi solved an important problem. It proved that open lending markets can be built on shared infrastructure and coordinated without a central operator.

But open lending and confidential credit are not the same thing.

On most public chain systems, transparency is a default condition. Positions can often be observed. Collateral movements can be tracked. Behavior under stress can become visible in real time. Participation is usually open. That works well for permissionless markets where openness is part of the design goal. It works far less well for institutions that cannot treat financing activity, strategic rebalancing, or counterparty relationships as public information.

That does not mean public DeFi is broken. It means it is optimized for a different type of market.

For institutions, the limitations of transparent lending often include:

- Strategy leakage through visible borrowing and collateral activity

- Counterparty ambiguity in fully open participation environments

- Shared risk exposure across markets with very different asset profiles

- Operational friction when privacy and controls need to be layered on afterward

In transparent lending environments, visible positions and predictable thresholds can also turn risk into public signal. Once that signal exists, the rest of the market can optimize against it.

That is an architectural difference, not a product surface one.

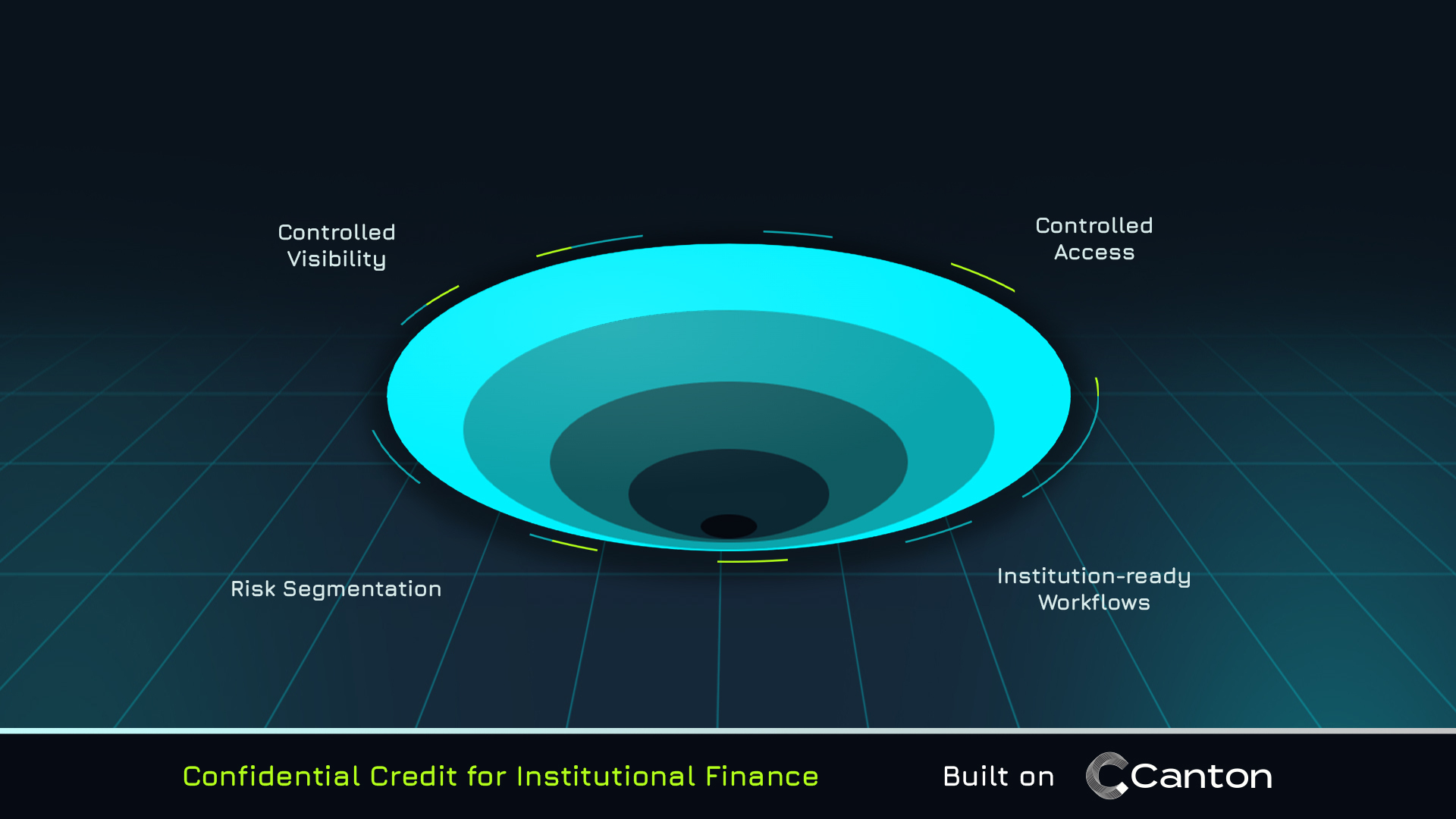

What Makes Credit Confidential

The four properties that define confidential credit: controlled visibility, controlled access, risk segmentation, and institution-ready workflows.

Confidential credit starts from a different architectural premise. Rather than assuming that all market activity should be visible unless hidden later, it assumes that visibility, participation, and risk boundaries should be designed intentionally from the outset.

In practice, confidential credit is defined by four core properties:

- Controlled visibility: relevant parties can see the information they need, but market activity is not broadly exposed by default

- Controlled access: participation can be governed rather than left fully open to unknown counterparties

- Risk segmentation: different markets, assets, and borrowers can operate under distinct rules and parameters

- Institution ready workflows: privacy, permissioning, and operational controls are built into the architecture rather than added later

This is the key distinction: confidential credit is not just lending with fewer dashboards. It is lending infrastructure designed for markets where information flow itself is part of product design.

Confidential credit also does not mean secrecy. It means structured visibility.

In a well-designed confidential credit market:

- Lenders see what they need to assess risk

- Counterparties see what they need to transact

- Regulators retain appropriate audit access

- Positions, strategies, and risk thresholds are not broadcast to the entire market

Serious credit markets do not broadcast risk to everyone by default. They route information to the parties who need it.

Confidential Credit Is Not Opacity

It is worth being direct about the obvious counterargument: confidentiality without accountability is opacity, and opacity in credit markets has historically enabled hidden leverage, mispriced risk, and systemic blind spots.

Confidential credit only works when paired with audit access, regulatory visibility, and clear governance. That is precisely why these properties are designed in rather than bolted on. The goal is not to remove oversight. It is to ensure oversight is routed to the parties who need it, while preventing market activity from being broadcast to participants who would simply trade against it.

Structured visibility is not the absence of accountability. It is accountability allocated correctly.

Why Institutions Need Confidential Credit

Institutions do not evaluate lending infrastructure the same way a retail DeFi user does.

They are not only asking whether they can borrow or earn yield. They are also asking whether the market structure fits how they are permitted to operate. In practice, that usually means evaluating questions such as:

- Can positions and collateral activity remain private where needed?

- Are counterparties known, governed, or otherwise controlled?

- Is risk segmented cleanly by market and asset?

- Can liquidation and enforcement happen without unnecessary information leakage?

- Does the infrastructure fit regulated operating environments?

Consider a treasury desk that wants to borrow against a tokenized bond portfolio to meet a short-term liquidity need. On a transparent rail, the borrowing action itself signals funding pressure, the collateral composition reveals portfolio strategy, and the liquidation threshold becomes a target for other market participants. On a confidential rail, the same transaction is executed with visibility limited to the counterparties and regulators who need it.

That is why confidential credit matters. It expands the set of financial actors and use cases that can realistically move onchain.

If the only model available is transparent-by-default lending, then the addressable market stays narrow. Some forms of open crypto credit can thrive, but institutions with real balance sheets remain constrained by the assumptions of the rail itself. If the infrastructure instead supports confidentiality, controlled interoperability, and institution-grade market design, then a much broader class of credit activity becomes possible.

Why the Underlying Rail Matters

A market can only be as institution ready as the infrastructure it runs on.

If the underlying environment assumes radical transparency, then privacy becomes an exception to the rule. If the environment assumes fully open participation, then access control has to be layered in awkwardly. If applications can only interoperate by exposing too much information, then sensitive financial workflows remain constrained.

Canton takes a different approach. It is a privacy-enabled open blockchain designed for regulated financial markets, where assets and data move across applications with real-time synchronization while preserving the controls institutions require. This is achieved through Canton's sub-transaction privacy model, in which participants only see the parts of a transaction relevant to them, privacy as a property of the architecture, not a feature applied on top.

That makes Canton a natural substrate for confidential credit. Cenote's positioning follows the same logic: Canton was designed from the outset for regulated financial workflows, privacy is part of the architecture rather than a workaround, and Cenote is building private, compliant lending natively on that stack.

How Cenote Is Building Confidential Credit on Canton

Cenote is building confidential credit infrastructure on Canton - privacy, controlled participation, and segmented risk built into the architecture.

This is where we fit.

We believe institutional finance needs confidential credit, not just generic lending. That means building infrastructure around compliant privacy, institutional credit, isolated markets, governed access, and privacy-preserving market design.

Looking ahead, our architecture is designed to treat staking and lending as reinforcing parts of the same system. A planned component, sCC, is intended to function as a yield-bearing asset powered by validator rewards and usable as lending collateral within Cenote's markets. We see market structure, collateral design, and capital formation as linked problems, which is reflected in how the broader protocol is being built.

Our goal is not to wrap public chain money markets in more institutional branding. It is to build lending infrastructure that reflects the actual operating conditions of institutional finance on Canton.

That is also why the architecture matters. We are building on infrastructure designed for regulated financial workflows, where privacy is part of the system design rather than a workaround added later.

More broadly, we see confidential credit as the missing layer between open blockchain infrastructure and the kinds of credit markets institutions can actually use.

In Short: What Is Confidential Credit?

Confidential credit is onchain lending infrastructure built for markets that require:

- Privacy

- Controlled participation

- Segmented risk

- Institution-grade workflows

Public lending proved that credit can exist onchain.

Confidential credit is about making it usable for institutions.

That is what Cenote is building on Canton.

Coming next

In the next post in this series, we'll go deeper on Isolated Lending Markets, why segmenting risk by market, asset, and participant set is foundational to confidential credit, and how isolated market design protects institutions from the shared pool risk dynamics that have shaped public DeFi lending to date.