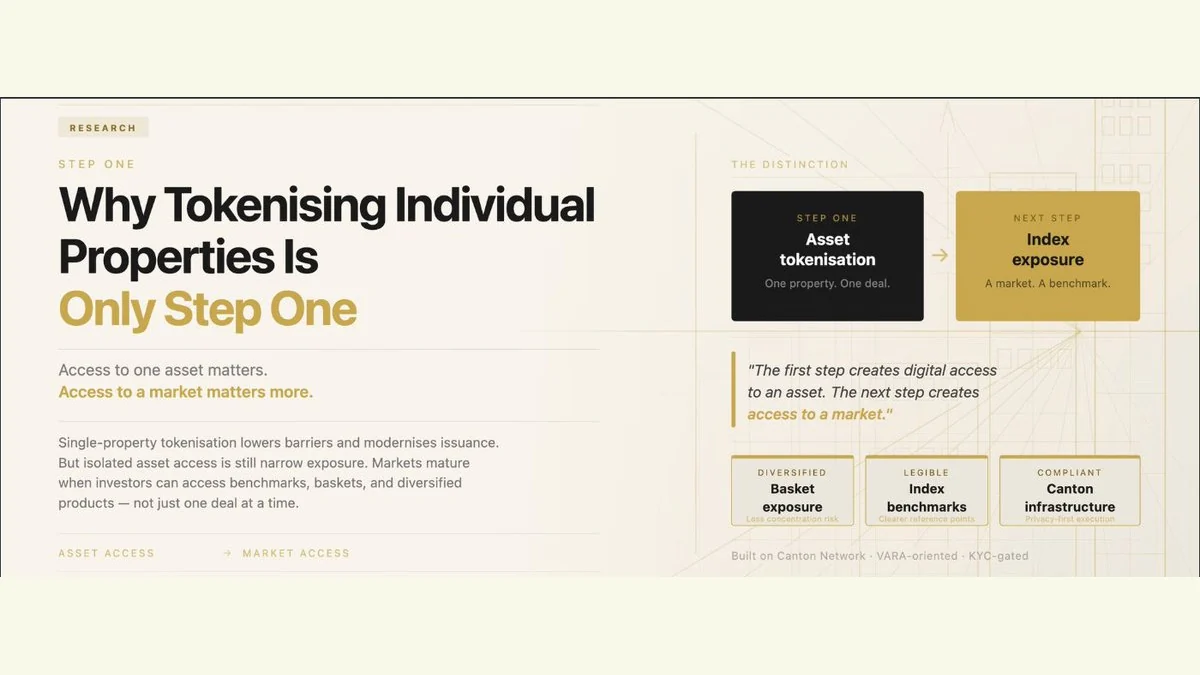

Access to one asset matters. Access to a market matters more.

Single-property tokenisation is an important starting point for real-estate markets on-chain.

It can lower entry barriers, make ownership more divisible, and create a cleaner digital wrapper around real-world exposure. It also helps modernize parts of issuance, transfers, and compliance workflows that are often slow and fragmented in traditional structures.

That progress matters. But it is not the full answer.

The deeper question is not whether one property can be tokenised. The deeper question is whether investors can access real-estate markets in a form that is diversified, legible, and investable.

That distinction is critical.

A tokenised apartment, office, or building gives exposure to a specific asset. It may reflect one location, one sponsor, one tenant profile, one capital structure, and one local market cycle. That can be useful, but it is still narrow exposure.

Most capital markets do not scale through isolated assets alone.

Public equities did not become widely investable because investors could buy one company at a time. They matured because markets developed benchmarks, baskets, sector exposure, and products that made allocation simpler. Fixed income evolved the same way. Real-estate markets on-chain are likely to follow a similar path.

That is why single-asset tokenisation should be seen as step one, not the finished product.

The first step creates digital access to an asset. The next step creates digital access to a market.

That is where the opportunity becomes more meaningful.

Market access is different from asset access. Asset access allows an investor to buy into one deal. Market access allows an investor to express a broader view — on a city, a segment, a region, or a benchmark. It turns fragmented exposure into something more structured and more understandable.

This matters because many investors are not looking to underwrite one building. They are looking to allocate capital to a theme, a geography, or a sector with more clarity and less concentration risk.

That shift changes how products should be designed.

Instead of asking whether a single property can be tokenised, the more relevant question becomes: can real-estate indexes and baskets be brought on-chain in a way that preserves clarity, compliance, and credible exposure?

That is the direction now emerging at Fractit.

The focus is shifting from tokenised real estate in its narrowest form toward bringing real-estate index exposure on-chain through infrastructure designed for privacy, compliance, and institutional-grade execution.

This is not just a product decision. It is a market-structure decision.

Single-property tokenisation can expand access to deals. Index-based exposure can expand access to markets.

That difference matters because markets become more useful when investors can do more than buy isolated assets. They become more useful when investors can allocate, compare, rebalance, and build exposure with clearer reference points.

Real-estate tokenisation still has significant room to evolve. One of the clearest next steps is moving from one-off assets toward products that make the market itself investable.

That is the problem space Fractit is building in.